172

ANNUAL REPORT 2016

NOTES TOTHE FINANCIAL STATEMENTS

30 JUNE 2016

(Continued)

37. FINANCIAL INSTRUMENTS (continued)

(e)

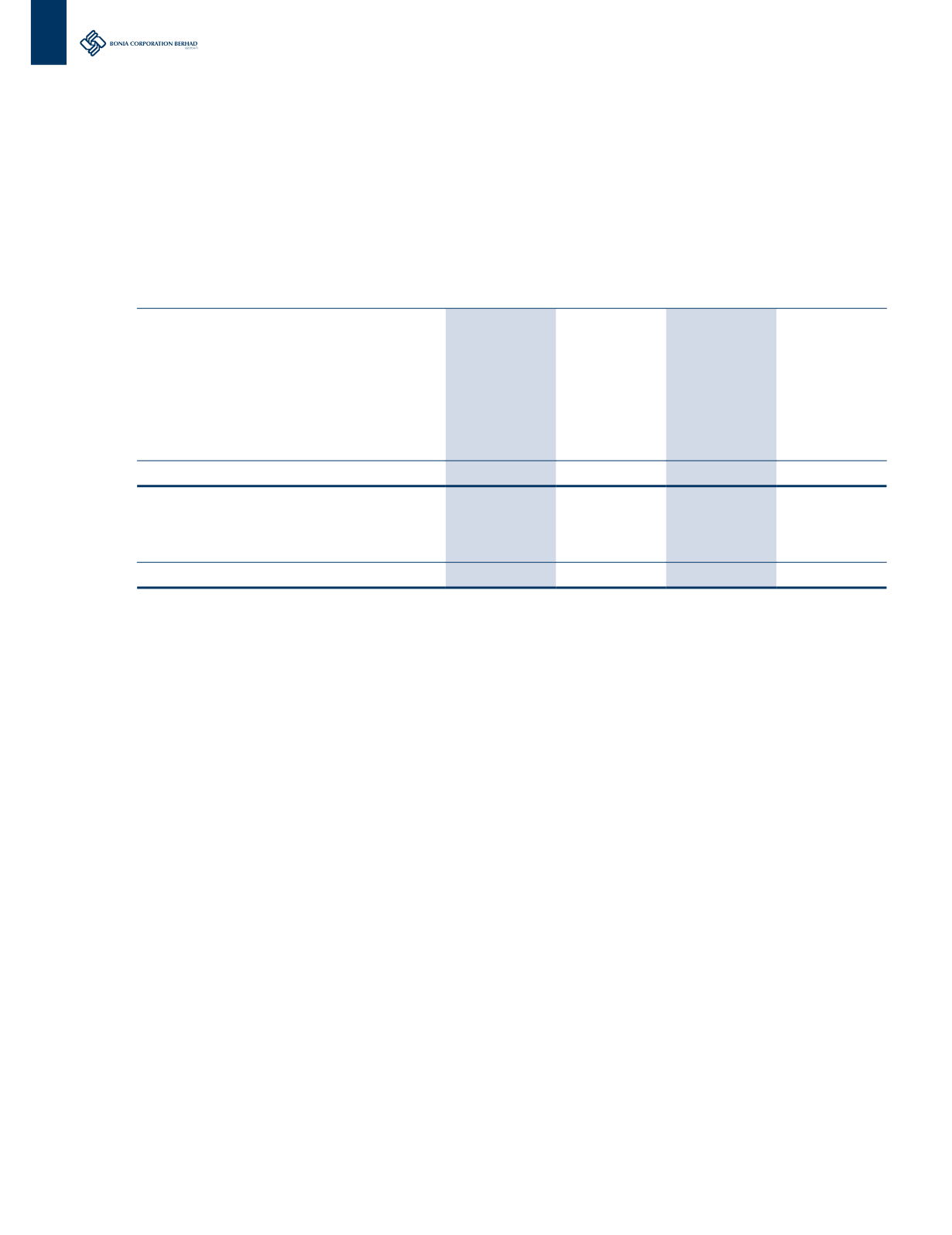

The following table shows a reconciliation of Level 3 fair values:

Group

Company

2016

RM’000

2015

RM’000

2016

RM’000

2015

RM’000

Financial assets

Balance as at 1 July 2015/2014

1,137

1,099

-

-

Additions

189

-

-

-

Disposal

(36)

-

-

-

Fair value loss recognised

(25)

-

-

-

Translation adjustments

33

38

-

-

Balance as at 30 June 2016/2015

1,298

1,137

-

-

Financial liabilities

Balance as at 1 July 2015/2014

-

-

-

-

Acquisition of a subsidiary

13,678

-

-

-

Balance as at 30 June 2016/2015

13,678

-

-

-

Sensitivities for the Level 3 fair value measurements of the financial assets and financial liabilities are not disclosed as they are not

material to the Group.

38. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

The financial risk management objective of the Group is to safeguard the shareholders’ investment and the Group’s assets whilst minimising

the potential adverse impact arising from fluctuations in foreign currency exchange and interest rates and the unpredictability of the

financial markets.

The Group operates within an established risk management and internal control framework and clearly defined guidelines that are regularly

reviewed by the Board of Directors. Financial risk management is carried out through risk review programmes, internal control systems,

insurance programmes and adherence to the Group financial risk management policies. The Group is exposed mainly to credit risk, liquidity

and cash flow risk, interest rate risk and foreign currency risk. Information on the management of the related exposures is detailed below.

(i)

Credit risk

Cash deposits and trade receivables could give rise to credit risk, which requires the loss to be recognised if a counter party fails to

perform as contracted. The counter parties are major international institutions and reputable multinational organisations. It is the

policy of the Group to monitor the financial standing of these counter parties on an ongoing basis to ensure that the Group is exposed

to minimal credit risk.

The primary exposure of the Group to credit risk arises through its trade receivables. The trading terms of the Group with its customers

are mainly on credit, except for boutique sales, where the transactions are done in cash term. The credit period is generally for a

period of 30 days, extending up to 120 days for major customers. Each customer has a maximum credit limit and the Group seek to

maintain strict control over its outstanding receivables to minimise credit risk. Overdue balances are reviewed regularly by senior

management.