159

ANNUAL REPORT 2016

NOTES TOTHE FINANCIAL STATEMENTS

30 JUNE 2016

(Continued)

34. RELATED PARTIES DISCLOSURES (continued)

(c)

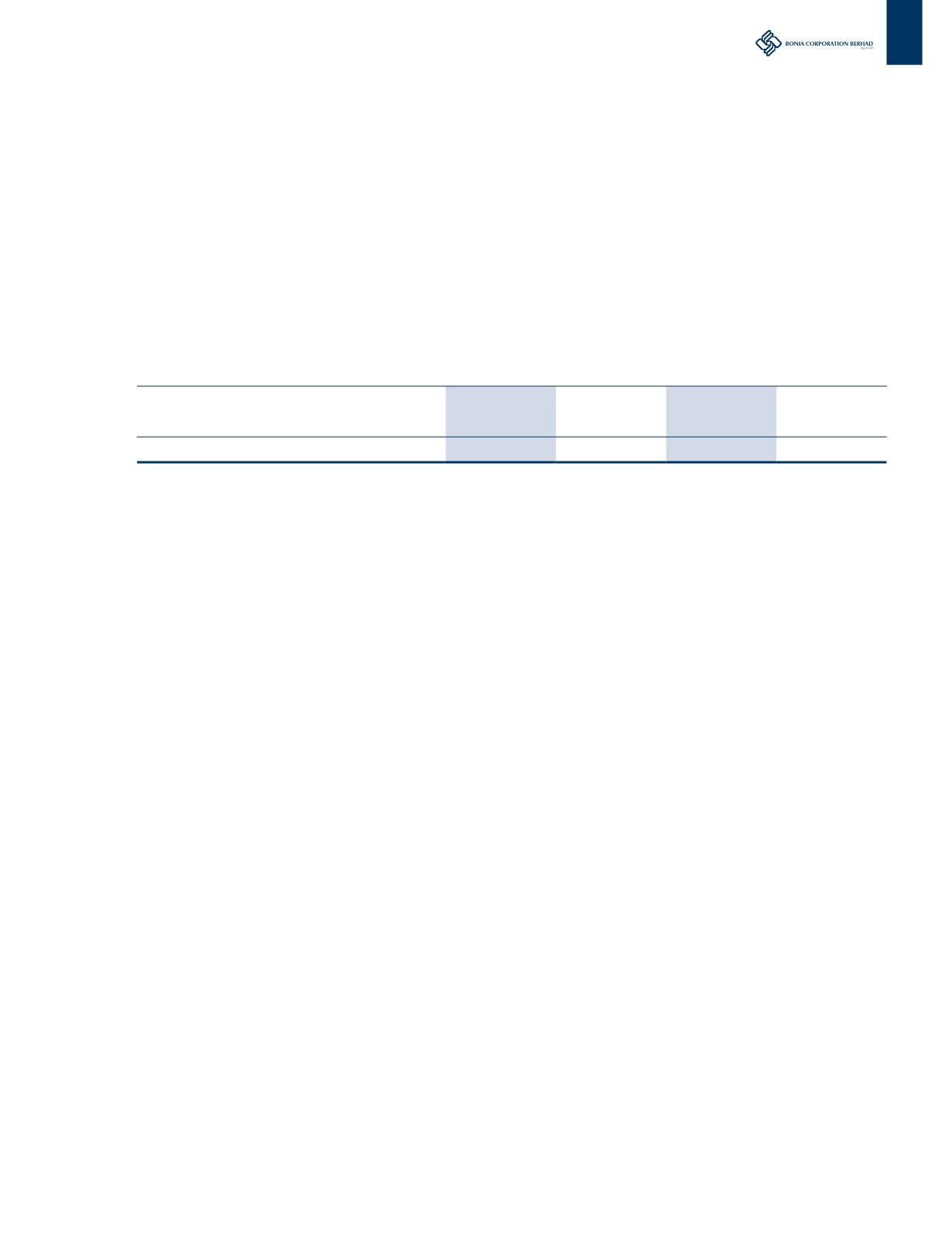

Compensation of key management personnel

Key management personnel are those persons responsible for planning, directing and controlling the activities of the entity, directly

and indirectly, including any director (whether executive or otherwise) of the Group and of the Company.

The remuneration of Directors and other key management personnel during the financial year was as follows:

Group

Company

2016

RM’000

2015

RM’000

2016

RM’000

2015

RM’000

Short term employee benefits

13,332

19,472

1,857

3,998

Contributions to defined contribution plan

1,270

1,709

194

461

14,602

21,181

2,051

4,459

35. ACQUISITION AND DISPOSAL OF SUBSIDIARIES

(a)

On 29 January 2016, Jeco had entered into a Sale and Purchase Agreement (“SPA”) with Helgo Neugebauer (“HNB” or “Seller”), an

unrelated party to acquire 100 ordinary shares of SGD1.00 each, representing 100% of the entire issued and paid-up capital of IBB

at a total cash consideration of SGD6,000,000. The acquisition was completed on 15 February 2016 (“Completion Date”) and IBB

became a subsidiary of the Group. The salient terms of the SPA are summarised as follows:

The cash consideration is payable in the following manner:

(i)

SGD1,000,000 is payable to the Seller within 1 month from the Completion date;

(ii)

SGD2,500,000 is payable to the Seller on 30 April 2017 subject to the receipt of Audited Accounts 2016 of IBB (“First Post-

Completion Payment”); and

(iii) SGD2,500,000 is payable to the Seller on 30 April 2018 subject to the receipt of Audited Accounts 2017 of IBB (“Second Post-

Completion Payment”)

In turn, IBB should achieve an audited aggregate profit after tax (“profit guarantee” or “contingent consideration arrangement”) as

warranted by HNB as follows:

(i)

at least SGD2,000,000 audited profit after tax for the financial period of 1 January 2016 to 31 December 2016, failing which

the shortfall should be deducted from the First Post-Completion Payment;

(ii)

at least SGD2,000,000 audited profit after tax for the financial period of 1 January 2017 to 31 December 2017, failing which

the shortfall should be deducted from the Second Post-Completion Payment;

(iii) If the audited aggregate profit after tax for the financial period of 1 January 2016 to 31 December 2017 is at least SGD4,000,000,

the total amount deducted from the First Post-Completion Payment or Second Post-Completion Payment, as applicable, should

be paid to HNB on 30 April 2018; and

(iv) If during the financial period of 1 January 2016 to 31 December 2017, the Indonesian Rupiah (IDR) depreciated more than

20% from the foreign exchange rate against the SGD as at Completion Date, and the audited aggregate profit after tax for the

financial period 1 January to 31 December 2017, is less than SGD4,000,000, Jeco agreed that the total amount deducted

from the First Post-Completion Payment or Second Post-Completion Payment, as applicable, should be paid to the Seller on

30 April 2019 if the audited aggregate profit after tax for the financial period 1 January 2016 to 31 December 2018 is at least

SGD4,000,000.

As at the acquisition date, the fair value of the contingent consideration was estimated at RM13,678,000.